Many people think that the only way to build wealth is with a job. While it’s a great way to earn more money, it’s not the only way.

In fact, there are a lot of ways you can make your money work for you to build a Rich Life. With the right systems, you can save and invest for your future. Doing so will build a solid foundation for your personal finances.

Luckily, I know those systems. That’s why I’m going to show you the six best money tips that can help you pay off your debt, invest and grow your money, and save for something fun — like a vacation — this year.

- Money tip #1: Eliminate your debt

- Money tip #2: Invest in a 401k

- Money tip #3: Invest in a Roth IRA

- Money tip #4: Automate your finances

- Money tip #5: Leverage sub-savings accounts

- Money tip #6: Use target-date funds

Let’s get started.

How to make your money work for you — with 6 tips

These six money tips are going to leverage something I like to call Time Machine Investing.

No, I don’t have a flying Delorean — but I do have more than a decade of teaching people about personal finances.

Hop in, and leave your budget behind. Where we’re going, we don’t need budgets.

Money tip #1: Eliminate your debt

If you have debt, your first order of business is to get rid of it. Your money can only work for you once you’re out of debt.

After all, you can’t properly invest in yourself or your future if you have a mountain of credit card debt that you haven’t addressed yet.

Debt is one of the most common roadblocks keeping people from success. That’s why I don’t allow anyone with debt to take part in any of my flagship courses, costing us millions each year.

We don’t come out of the womb knowing how credit cards work. There’s no “Paying off your loans 101” class in high school. And credit card companies aren’t trying to help you. In fact, they’re in the business to keep you in debt for as long as possible so THEY can make money.

Luckily, there are steps you can take to get out of debt no matter how much you owe.

I wrote an article detailing exactly how you can get out of it. Here are the key insights from that article:

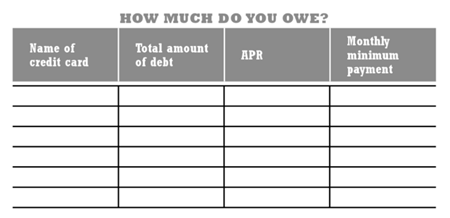

- Find the exact amount you owe. A study found that many don’t actually know how much debt they owe. However, this just leads to you blindly paying the minimum payment instead of actually owning your debt. Only then can you start a good strategy to get rid of it.

- Utilize the Snowball Method. Dave Ramsey famously touts his Snowball Method of getting out of debt. This involves paying the minimums on all of your debt, but paying more money to the card with the lowest balance first (i.e., the one that will allow you to pay it off the quickest).

- Decide how you’re going to pay your debt. There are a number of ways you can approach this. You can negotiate a lower interest rate and put the money you save toward chipping away at what you owe. You can also tap into hidden income to free up some money. If you’re really enterprising, though, you can start EARNING more money.

First step: Go through your account statements, call the companies, do whatever it takes to find out how much you owe on these bills. You can use this tool to track it (it’s the second link on this list). The chart looks like this:

It’ll help you find out how much you owe to each company and what your interest rates are. You can also use my free online tool here.

Stop right now and do this.

Done?

Congrats! Taking the first step is one of the hardest parts — now you’re well on your way to a Rich Life.

If your total debt number seems high, remember two things:

- There is a large group of people with more debt than you.

- From this day that number is only going to go down. This is the beginning of the end.

If you need help getting out of debt, check out my absolute best resources on getting out of debt below:

- How to improve your credit score

- How to get out of debt fast

- How to use credit cards to rebuild credit

BONUS: For even more systems on eliminating your debt, check out my 3-minute video below on how to negotiate your debt.

Money tip #2: Invest in a 401k

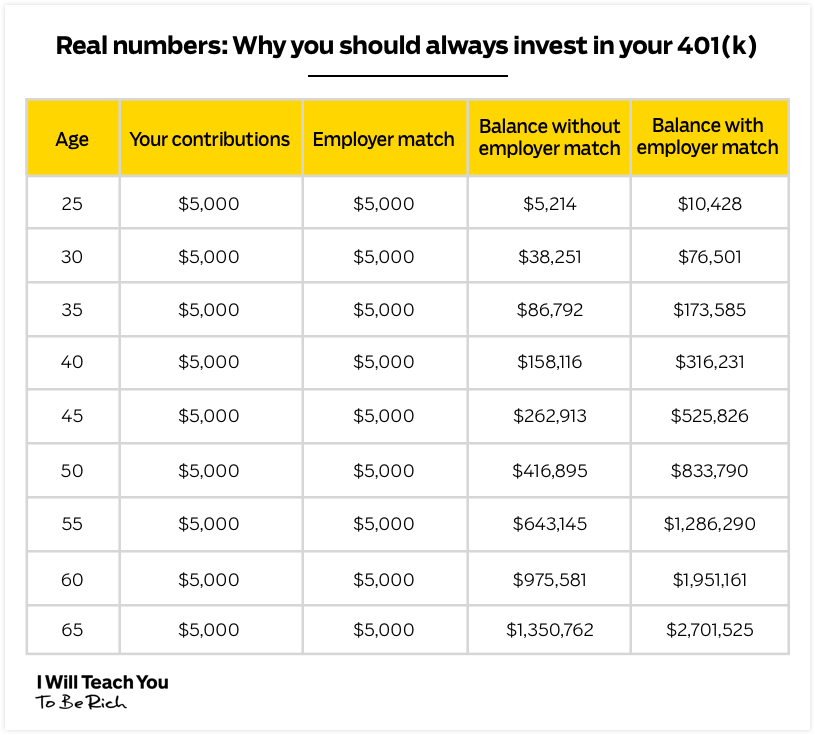

A 401k allows you to invest money for retirement AND receive free money from your employer while doing so.

Here’s how it works: Each month, a portion of your pre-tax pay is invested automatically into the 401k. If you hit a certain percentage of contributions, your employer will also match you 1:1.

You aren’t taxed on your earnings until you withdraw it at retirement age (59 ½ years old). This means that you’ll earn more with compounding over your lifetime.

Imagine you earn $100,000 / year and your company offers you a 3% match on your 401k. If you invest $3,000 (3% of $100,000), your company will match you that much in your 401k. You can contribute more — but your company won’t match you beyond 3%.

Currently, the contribution limit for a 401k is $18,500. Maxing it out is an awesome goal to have.

Be sure to take advantage of your employer’s 401k plan by putting at least enough money to collect the employer match into it. This ensures you’re taking full advantage of what is essentially free money from your employer. That match is POWERFUL and can double your money over the course of your working life:

For more on 401ks, be sure to check out my article on the topic here.

Money tip #3: Invest in a Roth IRA

This is another tax-advantaged retirement account that allows for incredible growth and savings.

Unlike your 401k, though, this account leverages after-tax income. However, you’re not taxed on your earnings when you withdraw it at retirement age. AWESOME.

Like your 401k, you’re going to want to max it out as much as possible. The amount you are allowed to contribute goes up occasionally. As of 2018, you can contribute up to $5,500 / year.

I suggest putting money into an index fund such as the S&P 500 as well as an international index fund as well.

For more information about Roth IRAs, be sure to check out my article on them here.

Note: If you don’t know where to find the money to invest in these accounts, read all the ways you can free up that money with just a few phone calls.

Money tip #4: Save automatically

The best time to grow a tree is 10 years ago. The second best time is today.

I know, I know. I sound like a cheesy motivational poster — but the adage is true.

If you want to buy a house or a nice car one day, you don’t want to think about where you’re going to get the money the day you plan to buy it. You want that money to already be there.

That’s why I’m a HUGE proponent of automating your finances.

There are still people out there who have heard me harp on this for literal YEARS and still haven’t automated their finances. And why not? For a few hours of work, you can save yourself thousands of dollars down the road.

One reason many are averse to saving money is due to the pain of putting our hard-earned cash into our savings accounts each month. That’s why we turn to automation. It’s a set-it-and-forget-it approach to your finances, allowing you to send all of your money exactly where you need it to go as soon as you receive your paycheck.

After all, if you had to track your spending and move money into savings every month, it would eventually be one of those “I’ll get to that later…” things and you’d NEVER get to it.

And so, just like cutting out luscious, perfectly foamed 12 Corners lattes, we might put away money for savings once or twice — but if we have to make the decision EVERY paycheck, we’re setting ourselves up to fail.

That’s why automated finances work so well. You can start to dominate your finances by having your system passively do the right thing for you. Instead of thinking about saving every day — set it and forget it.

To do this, you need just one hour today to set everything up so your paycheck is divided into four major buckets as soon as it arrives in your checking account. They are:

- Investments: I highly suggest you put your money into a Roth IRA. Like your 401k, you’re going to want to max it out as much as possible. The amount you are allowed to contribute goes up occasionally. Currently you can contribute up to $5,500 each year.

- Savings: Here, you should use “sub-saving accounts” that you’ve created for long-term goals like your wedding, vacation, or down payment on your house. Many banks provide the option to create smaller sub-accounts in your normal savings account — perfect for goal setting.

- Guilt-free spending: Make automatic payments for recurring services like Netflix, Birchbox, and gym memberships using your credit card. You’re going to have plenty of guilt-free spending money in here for things like the occasional night out or fun purchases you want to make.

Be sure to log into your credit card’s website and set up automatic payments with your checking account so your credit card bill is paid off each month. You can rest assured that you will have enough money in your checking because you’ve already set up automatic payments with everything else.

- Fixed costs: These are for bills that can’t be paid off with a credit card, such as rent, electric, water, and gas.

Once that money is in your savings account, don’t touch it unless you’re ready to pay for your long-term goal (or if there’s a HUGE emergency).

For more information on how to automate your finances, check out my 12-minute video where I go through the exact process with you. (Try not to be too impressed with my awesome whiteboard art.)

Money tip #5: Use sub-savings accounts

Once you automate your finances, you can optimize your savings by leveraging a sub-savings account.

This is a savings account that you can create within your regular savings account to save for specific purchases or events.

Each month, you can automatically transfer your money into these accounts. Once the transfers are in place, you’re going to get a lot closer to your savings goals. AND you can do it without having to remember to set money aside.

Check out all the different sub-savings accounts I had in my old savings account:

ING Direct is now Capital One 360. BTW that wedding one was put to good use.

Here’s a look at a few sub-savings accounts I have now:

ING switched to Capital One 360. I used the money I saved to buy an engagement ring.

So set up a sub-savings account and start automatically putting money into it each month. If you need help, check out my article all about sub-savings accounts to get started.

This is an example of using a system to make sure you have the money needed for an expensive purchase. These sub-savings accounts can be for a new car, a new wardrobe, a trip you want to take … anything at all.

You can even set aside money for more nebulous things. See my “stupid mistakes.” Or maybe you can have a “for when my buddy insists on ‘just one more drink’” account.

Now, each time I want to spend money on an expensive purchase, I KNOW I have the money. Because I have been storing a little bit at a time automatically. And I can make the purchase stress-free.

Money tip #6: Use target-date funds

Target-date funds (or lifecycle funds) are a collection of assets that automatically rebalance and reallocate themselves as time goes on. They’re a great way to save for retirement if you don’t want to deal with choosing your portfolio mix.

Target-date funds diversify based on your age. This means the funds will automatically adjust to be more conservative as you get older.

For example, if you want to retire in 30 years, a good target-date fund would be the Vanguard Target Retirement 2050 Fund (VFIFX), since 2050 will be close to the year you’ll retire.

If you invest in this fund today, the investments will be much more aggressive. This means it’ll be higher risk but with the potential for greater returns. As the years pass and we inch closer to 2050, though, the fund will automatically adjust to invest in more conservative investments like bonds.

Most target-date funds require a $1,000 to $3,000 initial investment. If you don’t have enough to invest in one of those, don’t worry. Check out my article on earning more money to get the investment this month.

In all, these are fantastic funds for anyone looking for an automatic, painless way to invest for retirement.

Invest in a Rich Life

If there’s one thing that I hope my readers have gained from my blog, it’s that you should always be in a state of curiosity. Be inquisitive. Ask questions when you don’t understand something and don’t be afraid to seek out more information through books, courses, or schooling. It’s only then that you can hope to truly live your Rich Life.

And don’t just focus on things that you think are closely related to your career. I want you to approach education laterally. You’ll be surprised at the things you’ll be able to pick up that’ll help you in life and at the office.

- Are you an investment banker? Go take an improv class and become better at public speaking (and cracking jokes with others).

- Small business owner? Take a course in another language like Spanish or French. You might be able to broaden your audience that way.

- Aspiring baker? Join that cool sci-fi writing workshop you saw online. At the very least, you’ll be able to craft solid business proposals.

Your thirst for education should be constant and voracious. I don’t care if you’re reading this in your 20s or your 60s. There’s always something new to learn that you can add to your well of knowledge to draw upon.

Want more lessons from this time machine? I have an offer for you: My Ultimate Guide to Personal Finance.

In it, you’ll learn how to:

- Master your 401k: Take advantage of free money offered to you by your company … and get rich while doing it.

- Manage Roth IRAs: Start saving for retirement in a worthwhile long-term investment account.

- Automate your expenses: Take advantage of the wonderful magic of automation and make investing pain-free.

6 easy ways to make your money work for you is a post from: I Will Teach You To Be Rich.

Via Finance http://www.rssmix.com/

No comments:

Post a Comment